Thank you for this beautiful explanation, just note the royalties are received by James and not paid by James

A

Aditya·

actually the impact of royalties is irrelevant. Royalties are first being converted in EUR as outflow, then taxed at 20%, being converted back into GBP and then additionally taxed at 5%. If you calculate, you'll get the net outflow of 75 after all of this (For example Year 1- Outflow in EUR is -115 causing a tax saving of EUR 23, making the net outflow to be -92 - converted to GBP is GBP 80. Then additional 5% on 115 = . , then we show 75 (100 less 25% tax) as inflow for James. If you remove Royalties from your calculations altogether, you'll get the same net cashflow. Its a matter of presentation and has no impact on the cashflows at all

J

John MoffatTutor·

See my reply to the previous question (immediately below).

I

Inam·

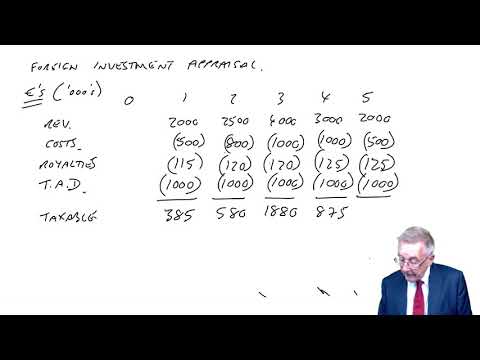

Since it’s mentioned in the question that an amount equal to the amount of the tax allowable depreciation is required each year for the maintenance of non-current assets.

While you mentioned that the trick to tackle this is to when you compute the tax allowable depreciation for the purpose of arriving at the Taxable profit in order to figure out the tax expense on the profit, so don’t add back the same after figuring out the tax expense.

However, excluding maintenance expenses when calculating taxable profit can lead to discrepancies in our NPV and cash flow projections. Maintenance expenditure is tax allowable, and it should be kept alongside depreciation before the taxable profit.

For instance, if we were to incorporate maintenance expenses of 1,000 Euro annually in addition to depreciation, it would result in taxable losses, thereby reducing our tax liability. Neglecting these maintenance expenses before arriving at taxable profit inflates the taxable profit figure, consequently leading to higher tax payments.

So why you have not account for the maintenance expenses even it’s cashlfows in your table before arriving the taxable profit?

J

John MoffatTutor·

You make a perfectly valid point. However the current examiner never treats it as being tax allowable which is why I show it the way I do in my lectures.

I

Inam·

Thank you so much for the response.

Just to re-ensure that in case in exam it's being mentioned that an amount equal to the amount of the tax allowable depreciation is required each year for the maintenance of non-current assets. So in such case we wouldn't subtract the maintenance expense to arrive at taxable profit and neither we will add back the tax depreciation after arriving at the taxable cashflows.

However, now do have one more curiosity ? What if in exam it's being mentioned that an amount of XXX (any amount but different to that of depreciation) is required each year for the maintenance of non-current assets. So in such case we would still follow the same treatment as carried out by you?

Furthermore, would take this moment to appreciate your energy for replying to our's queries.

J

John MoffatTutor·

Your stating of the 'rule' is correct.

If he had different amount then he would have to make it clear about the tax position.

S

Swati·

HI there,

Thank you for the lectures and notes.

I just had one doubt and that is, in the question its mentioned that "An amount equal to the amount of the tax allowable depreciation is required each year for the maintenance of non-current assets" so for calculating the tax it will be required to deduct the depreciation as well as the maintenance of the same amount from the revenue, that is an amount of 2,000 (1000 for dep, and 1000 for the maintenance). However, as depreciation is non cash it will be returned back. Although, the net effect is same as mentioned but it will definitely affect the tax calculated.

Please explain if i am wrong.

Thank u in advance for clarifying the query.

J

John MoffatTutor·

Strictly you are correct (the maintenance will be tax allowable). However the examiner includes this in almost every exam and always deals with it the way that I do in my lecture.

O

Oby·

Then why do we do the wrong. Whats the motive and justification

O

Oby·

U are correct.

M

Mohamed·

sir , thank you for the effort. one question why we counted royalties in the both? isn't it already calculated, implied in the totals and implied in cash? it looks now as received twice?

M

Mohamed·

implied in tax*^

A

Ann·

In example 4, why wasn't there a balancing charge/allowance in time 5 like in the previous examples?

Was it because the investment was in an operation and not a non-current asset?

Or was it because the operation was not sold/disposed off in Year 5 so there wasn't a balancing charge/allowance?

Or was it due to the straight-line method which doesn't produce a balancing charge/allowance?

J

John MoffatTutor·

It is because the question said to use 20% straight line tax depreciation together with the fact that there are no sale proceeds. So using the same tax workings as normal results in no balancing change or allowance.

A

Ann·

Am I right to comprehend that a balancing charge or allowance only arises when there are sale proceeds (when an asset is sold/disposed)?

A

Ann·

Residual value doesn't necessarily mean that an asset is sold?

J

John MoffatTutor·

It arises when the asset is disposed of, whether or not there are any sale proceeds. (If it is simply 'thrown away' then effectively the sale proceeds are zero, and so there will be a balancing allowance of any remaining tax written down value).

As far as the exam is concerned, the residual value is taken to be the sale proceeds.

B

Birju·

Hi Mr Moffat,

This is about rounding and rather that typing numers in the CBE versions of the exams, actually using the formula capability of the spreadsheet tool.

Feels like the mark schemes are rounding before the calculations are done.

Do you have any advice, its much quicker and more correct in practice if you dont round a number before calculating.

This problem naturally becomes greater as time periods increase and rely on previous numbers.

Best,

Birju

J

John MoffatTutor·

It doesn't matter whether you use the exact figures or whether you round them (usually to the nearest thousand) unless obviously the question specifies differently.

The marks in Section C are for the approach rather than for the final answer (and nobody cares either in the exam or in real life about a difference of a few hundred).

L

Luqman·

Is there any tip to know when I should be multiplying and dividing the figures/PV when translating from one currency to another?

J

John MoffatTutor·

This is explained in the first of the lectures on the management of foreign exchange risk :-)

L

Luqman·

I will check; thanks greatly

J

John MoffatTutor·

You are welcome :-)

M

Mr. Aboukar·

are there any occasions that we do not need to translate the net cash flows. is it must to always translate the net cash flows to parent's currency?

J

John MoffatTutor·

Given that it is the parent that will be making the decision, we will always translate to the parents currency.

M

Mr. Aboukar·

Got it.

Thank u very much

J

John MoffatTutor·

You are welcome.

P

piumiwijayasena·

I also think maintenance cost and depreciation cost both should be deducted to get the taxable profit. please explain !

J

John MoffatTutor·

It is a reasonable point. However this is something that the current examiner has in almost every NPV question. The depreciation itself is not a cash flow but given that there is an equal amount spent on maintenance it is correct to subtract the amount as a cash flow. There is an argument for subtracting both to get the taxable profit, but the examiner never does in his answers.

M

Mirafzal·

Are these lectures still relevant for the coming 2022 September exam? ACCA adding extra 20 marks for professionalism, how we learn that

J

John MoffatTutor·

Yes they are all relevant. The 20 marks for professionalism is not technical learning. It is dealt with in a chapter in our free lecture notes which also contains links to relevant resources on the ACCA website.

R

Ron·

Hi sir. Thank you for the lecture. Please may I ask, if the NPV is only +1, or +2, which is a small positive figure (very near to zero), is the project still acceptable by the company? Or is there any other comments regarding this?

Thank you.

F

faramental·

Hi Sir. Thanks for the great lectures. Although, may I ask. Why are we deducting the TAD before the taxable CF, instead of adding tax benefit after paying the taxes? Deducting 1000 depreciation every year would reduce the CF by a thousand. Isnt it actually an amount that is allowed for the tax purposes only? Depreciation is irrelevant for CF isnt it?

F

faramental·

Apologies, my bad. Missed out on other info.

G

Gert·

Good day Mr. Tutor

With the exams these days taken online using the computers, can we use the calculation options of formulas that the spreadsheet enables, such as =NPV() & =IRR() when calculating NPV etc. or do we still have to use the tables.

Please advise if this is possible or will we lose marks?

Thank you

J

John MoffatTutor·

In Section C questions you should indeed use the NPV and IRR functions in the spreadsheet (as explained in the final chapter of our free lecture notes). You would not lose marks if you do not use the NPV and IRR functions but it would mean spending more time.

However for Section A and B questions it is still important that you understand the NPV and IRR.

N

Naeez·

Sir one quick question,

Let’s say if we decide to add back the TAD within the computation, what plausible assumption that I should state for this. Pls advise.

J

John MoffatTutor·

You do not need to state an assumption!

N

Naeez·

Sir,

Then, will the examiner give me the full marks if I don't state the assumption for adding TAD back?

Thanks in advance for your explanation!

J

John MoffatTutor·

Yes. You are expected to add the TAD back unless the questions states that an equal amount is spent on the maintaining of the assets.

J

Judith·

Does the examiner still assume and take the position that the expense for asset maintenance should not be deducted as a separate expense ?

J

John MoffatTutor·

Yes. That is why I mention it in the lecture!!

J

John MoffatTutor·

We apply it to the taxable profits of Oblivia, and I have done. There is an extra 5% tax payable in the UK because the UK tax is 25% whereas the Oblivian tax rate is 20%.

G

GHULAM·

Sir,

If net cash will not be remitted to the UK then what will be the effect on the calculation of NPV? Secondly why we are deducting royalties above as we are making calculations from James Plc's point of view. Please advise.

J

John MoffatTutor·

If the cash was not remitted then it would be re-invested in Oblivia. This would earn more cash and at some stage there would be a remittance. If James was never going to be able to get any cash remittance they would not have invested.

The royalties are allowed for tax in Obvlivia but are taxable in the UK - the tax rates are different.

G

GHULAM·

Thank you Sir

D

Daniela·

Hi

In the Oblivia project, why weren't the Maintenance costs also deducted before taxable profits as this is a tax deductible expense and therefore reduce the tax liability? Then after tax calculation, add back the TAD? Although the cash flows would still net off, the tax liability would be different?

Thanks

D

Daniela·

Nevermind, I have read through the previous comments and realised you have already answered this question. Although I still don't understand why, I will take the advice from your replies.

Thanks :)

J

John MoffatTutor·

If you are referring to example 4, then there is no mention of any requirement for working capital in the question!

J

John MoffatTutor·

If the question does not mention working capital, then you cannot just invent it!!!

Y

YASH·

Hey john.

I have a question out of curiosity, what will happen if there wouldn't be any double tax treaty in the question?

What will be the tax treatment then?

Thanks for the great lectures.

J

John MoffatTutor·

There would then be full tax in the foreign country and full tax in the home country as well :-)

However in the exam questions there has always been a double tax treaty.

E

emily·

Sir I thought we use the higher of the two tax rates, meaning we would use 25% tax??? I'm confused.

J

John MoffatTutor·

They pay 20% tax in Oblivia to the Oblivian tax authorities.

In the UK they pay 25% tax, but because of the double taxation treaty they get credit for the 20% already paid in Oblivia and so just pay an extra 5% to the UK tax authorities.

A

Arunesh·

if the tax rate in uk was 20% and the tax in the foreign country 25%

would there be a 5% tax rebate?

J

John MoffatTutor·

No. There is no rebate, only extra tax if the tax rate in the home country is higher :-)

J

John MoffatTutor·

We are appraising the project in Oblivia, and the subsidiary in Oblivia has to pay royalties to James (which reduces the profit and therefore the tax payable, in Oblivia).

J

John MoffatTutor·

You are welcome :-)

A

amanlalshrestha·

Why didn't you deduct the maintenance expense to get the Taxable amount?

D

dosan·

yes that is also my question. shouldnt we deduct maintanance cost as well to get taxable profit?

J

julianleong·

What Aman is stating refers to the reduced tax from the lower taxable profit which should have deducted the maintenance as it is a real cash out.

J

jocelynjm·

Hi John, thanks heaps for the excellent lecture.

As you mentioned in the previous lecture, investment in a foreign country is different from buying a machine, losses can be carried forward for next year's tax calculation purpose.

Based on above, I have 2 questions regarding example 4

1. why the initial investment of (4545) GBP at time 0's can not be carried forward?

2. if at time 1, we have a loss, can it be carried forward for time 2's tax calculation?

Thank you very much in advance!

J

John MoffatTutor·

1. As per normal tax rules, the initial investment gives rise to tax allowable depreciation and it is this depreciation that is allowable for tax.

2. Yes - a loss at time 1 would be carried forward and reduce the taxable profit at time 2.

J

jocelynjm·

Got it. Many thanks!!

J

John MoffatTutor·

You are welcome :-)

S

Sheikh Hassan·

Hi john

what about the 4545 pounds which James Plc is wiring to Oblivia to start this project. Will it not has any tax implications in either UK or Oblivia.If so will it not have an impact on the value of outflow?

J

John MoffatTutor·

No - there are no tax implications under UK tax laws. If there ever were to be any then the question would have to say what they were, because this is not a tax exam :-)

L

lauram87·

Hi,

I only have one technical question regarding the Notes to the course. I can't find in the Answers section the solutions for Example 4, 5 and 6 under this chapter. I was actually doing a recap and wanted to check against the workings there and that's when i noticed.

Many thanks,

Laura

J

John MoffatTutor·

They are not in the answers section, but I do go through the examples in the lectures.

J

jeantang·

Hi John,

Thank you for the lecture! Just a question here - why there is a need to add back the depreciation in this case while you did not add back the depreciation in the last example in part 1?

Thanks!!

J

John MoffatTutor·

In example 1 we add back the depreciation because it is not a cash flow - the way we normally do it for Paper FM (was F9). It is subtracted in order to calculate the tax but is then added back because it is not a cash flow.

In example 4, we do not add it back because although it is not a cash flow, the question specifically says that an amount equal to the depreciation is needed for the maintenance of the assets.

As I say in the lecture, this is what the current examiner almost always writes as part of the question.

F

FIRDOSH·

Hello John,

I am a bit confused regarding depreciation.in the previous eg the depreciation was taken for 4 years wherese in this eg it has been taken for 5 years.

I have already posted a query in ask my tutor forus which i suppose u havent come across.

thanks

I love your way to tutoring

J

John MoffatTutor·

I did answer your post in the Ask the Tutor Forum earlier today.

The same rule has been applied in both examples. In Example 1 there is a scrap value at the end of 5 year, and the TAD in the 5th year is the difference between the sale proceeds and the tax written down value.

In Example 4, there is no scrap value (so the sale proceeds are zero) and therefore the TAD is the difference between the tax written down value and zero.

L

ljax·

Dear John,

It is stated that the amount equal to the amount of the tax allowable depreciation is required each year for the maintenance of non-current assets.

As I understand this amount is the cash item which Oblivia project has to spent on the FA maintenance. Means, this is the real expenses, which were spent by the company and could be deducted in the tax calculation in addition to TAD.

My Question is: Why during the tax calculation we didn't deduct 20% twice? on tme as TAD, and second time as expenses spent for maintainance

Thanks,

Pave

J

John MoffatTutor·

You make a very valid point. However rightly to wrongly the examiner in his answers makes the assumption that the 20% is only deducted once, which is why I do it that was in my lecture.

L

ljax·

Thank you very much!

J

julianleong·

Technically, the maintenance should be deducted to get a lower taxable profit which will lead to reduced tax. After which the CA can be deducted to get the "new taxable profit" and the respective tax and then add back the CA which will give the same results but still the reduced tax from the maintenance is not accounted for. How should we do this if we encounter this in the exam because I am sure it is wrong.

C

carnaud·

Hi Sir,

I am aunable to understand why the TAD is 1000 not 200 as it's generally calc. as

dep*TAD tax rate in this case

5000/5 = 1000*20% =200

Thank you

J

John MoffatTutor·

The initial cost is $5,000,000 and the question says that TAD is 20% straight line, which is therefore $1,000,000 per year.

What you are confusing is that the tax saved as a result of the TAD will be the tax rate (which is 25% and not 20% in the question) as applied to the $1,000,000.

This is happening here - the tax has been calculated on the profit after the TAD.

C

Cynthia·

Hello John,

I will really appreciate if you can help provide some clarification on how to calculate the average inflation rate for the data below.

Expected inflation rates

EU expected inflation rate: Next two years 5%

EU expected inflation rate: Year 3 onwards 4%

USA expected inflation rate: Year 1 onwards 3%

The actual question says "The current selling price of each component is €700 and this price is likely to increase by the average EU rate of inflation from year 1 onwards".

Thanks.

J

John MoffatTutor·

In future please ask this kind of question in the Ask the Tutor Forum, and not as a comment on a lecture.

The inflation rates are given in the question - calculating any sort of average rate is of no relevance at all.

If the current price is €700, then the price in 1 year will be 700 x 1.05.

The price is 2 years will be 700 x 1.05^2

The price in 3 years will be 700 x 1.05^2 x 1.03

From then on you multiply by 1.03 each year.

It may help you to watch the Paper FM (was F9) lectures on investment appraisal with inflation.

N

neha elsa·

When do we tax on the realisable value of non current assets?

N

neha elsa·

Dear Sir,

If the question says "Assume there is no tax relief '' , i believe we tax at their respective rates and not the difference. However, when taxing at the home country, do we tax on taxable profits or the Operating profit ( before capital allowance) ?

A question in the BPP textbook shows that we tax at Operating Profit and not taxable profits. Why so?

N

neha elsa·

When do we tax on the realisable value of non current assets?

J

John MoffatTutor·

We don't tax the realisable value.

I go through all the tax rules for the exam in my lectures.

J

John MoffatTutor·

By 'no tax relief' then I assume you are meaning no double taxation relief (which would be very unusual in the exam). Tax would normally be calculated on the operating profit but I cannot comment on a question in the BPP Textbook because I only have the BPP Revision Kit.

S

Sarosh Awan·

Dear Sir,

Please explain the following

A) The concept of Tax saving on Tax allowable depreciation as it was not discussed while solving Example 4

B) The Concept of Double tax treaty: What would have happened if there was no double tax treaty between Uk and Oblivia, We would have then taxed the cashflows as per the respective tax rates in both countries

C) Royalties: Why were they added separately to James plc cashflows when the Cashflows received from Oblivia were already net of the royalty payment to James plc and Why were they taxed at 25 % and not the incremental of 5%

J

John MoffatTutor·

A. You should remember from Paper PM ((was F9) that TAD can be dealt with in 2 ways - both giving the same result. In Paper PM is more common to calculate the tax on the cash flows ignoring TAD and then bring in the tax saving on the TAD.

The other way was to calculate the tax after subtracting the TAD, and then add back the TAD because it is not a cash flow. In AFM it is better to use the second way (as I have done in example 4). However the TAD is not added back, because although it is not a cash flow, the question says that an equal amount is needed for the maintenance of non-current assets. I explain about this in the lectures, and as I say in the lecture it is something the current examiner does in all NPV questions.

B. Yes - both sets of flows would have been taxed at the relevant rates. However in every singe exam question a double tax treaty has existed.

C. The royalties are an expense of the company in Oblivia and therefore reduce the Oblivia profits. They are income to James in the UK and are therefore taxed in the UK. This is standard tax rules as well as always being the caae in AFM questions.

S

Sarosh Awan·

Dear Sir,

Will the examiner always mention that an equal amount Is needed to maintain the non current asset If not can we assume and do our workings according to that?

J

John MoffatTutor·

These days, the examiner always assumes it in his answers (whether or not it is mentioned in the questions). As always, in AFM, state your assumptions and if they are valid then you will still get the marks even if different from the examiners answer.

S

Sarosh Awan·

Dear John,

In Q1 June 2015 named Yilandwe Co, the examiner has first deducted the TAD and then added it back later, The question does not state any thing about the same amount being used to maintain the non current asset. How should we deal such questions?

M

mitshu·

Hi, sir. As for example 4, if i do the calculation from £ to €? Is it acceptable?

Thank you.

J

John MoffatTutor·

I am not sure what you mean. You have to calculate the cash flows (and therefore the remittances) in €'s and then convert the remittances to Pounds because James is in the UK.

M

mitshu·

If i were to attempt this example in the first place, will work out ending with CF in euro since question request to valuing project in Oblivia.

Guess i simply 'ignored' cash surplus will be remitted to UK each year.

J

John MoffatTutor·

It is the UK company that has to make the decision about the project in Oblivia. This sort of question is common in the exam.

M

mitshu·

Alright. Got it. Thank you sir

K

Kaushik·

Hello John,

Why is the extra UK tax is calculated by dividing foreign exchange rates when we already converted it into pounds currency in the previous step ?

J

John MoffatTutor·

But the tax hadn't been converted and I calculated it from the foreign tax that had been paid.

M

mahesh727·

Hi John

In example 4, James Pls question we deducted € 1000 depreciation to arrive taxable profit. It’s clear. But shouldn’t we deduct another € 1000 as a maintenance cost to arrive taxable profit ? Question says an amount equivalent to depreciation is required each year to maintain non current assets, so it means in addition to depreciation (non cas expenses) there will be another € 1000 cas out each year for maintenance of non current assets.

Bit concern about the clear treatment as this will be checked in next exam as well

Thanks

J

John MoffatTutor·

You have a valid point, but the examiner always ignores this possibility - he always subtracts the depreciation, treats the remainder as being the taxable profit, but then does not add back the depreciation because the same amount is spent on maintaining the assets.

I

ishrath350·

Hi John

Still its not clear on what basis maintanance cost is excluded from the taxable profit calculation. If i include both maintainance and capital allowances for taxable profit calculation in my working will that be incorrect?

J

John MoffatTutor·

As I wrote before, what you are saying is sensible. However it would make sense to do what the examiner always does, to be sure of getting the marks.

S

Silvia·

Hi John

why is depreciation is not added back after it is used for tax calculation purposes for the purpose of NPV calculation this is not cash item? As far as I know depreciation is to be used only to reduce taxable base... so following that logic they should be added back.

thanks

J

John MoffatTutor·

I assume that you are referring to example 4.

The question says 'an amount equal to the amount of the tax allowable depreciation is required each year for the maintenance of non-current assets'. This is something that the current examiner has in most questions.

Therefore although depreciation is not a cash flow and is added back, there is a cash outflow of the same amount. Therefore the net result is no effect.

I do actually explain this in my lecture (because it is coming in the exam these days).

A

asher100·

Hi John

Why has the revenue from royalties been included twice in the answer? The royalty revenues were initially converted into GBP in the earlier part of the answer, and then included again at their GBP amounts.

A

asher100·

Apologies, meant to say the royalty revenues were initially shown at their Euro equivalent amounts.

J

John MoffatTutor·

It is because they are an expense for the foreign company but income for the 'home' company.

H

herafatima·

Hi John, a rhetorical question, assume that the tax rate in UK is 18%, and there exists a double tax treaty between UK and Oblivia, in regard to James plc, the net cash surplus has been taxed in Oblivia at 20%, when calculating the net cash flows is there any tax credit of the excess 2% paid in Oblivia, to be included in the cash flows of James plc?? If yes, then why and if no, then why.

Thanks, John :)

A

AJY·

OK so since we saved tax by deducting the TAD, why didn't we include the tax savings as a positive inflow in our analysis? $1000 x 20% in year one for instance? because I remember you explaining this in F9.

A

AJY·

Haaa.. I watched the F9 lecture again.. I got it!! It's less complicated this way.

J

John MoffatTutor·

I am pleased you have got it :-)

J

Jaros?aw·

Hi,

thank you very much for Your lectures they are very helpful.

I have a question regarding example 4 and the amount payable each year for the maintenance of non-current asset and its treatment for profit or loss purposes.

Could you please advise why they have not been included in calculation of profit? I thought they should be treated as an operating expense (I assume they have not been included in the "Operating costs" line as its amount exceeds the amount disclosed in that item).

Thank you in advance for Your answer

J

John MoffatTutor·

You make a valid point. Most AFM questions rely on making assumptions, and if you state your assumptions then you would still get the marks (even though the final answer would be different).

However, since the current examiner always makes the assumption that it is dealt with as I show in my lectures, it would be safest to always assume this :-)

J

Jaros?aw·

Thank You:)

J

John MoffatTutor·

You are welcome :-)

N

nevado·

Hi John,

Your lectures are great!

I did not quite get your answer... Would you be able to tell me what the examiner's assumption is? I still cannot see why this is not included in the profit calculation...

Many thanks in advance.

N

Nassem·

Hi Sir, many thanks for the lectures very helpfull. I am still confused about WDA, why we do not treat it sepratly? 5000*20%*20% and add back to the tax on operating profit?

T

Talha·

That's another way of calculating tax benefits i used this mathod in F9.

But now you have to use this one to calculate Taxable profits and to apply Tax rate when converting it from one currency to another.

This mathod is easier then the other one as calculations will go complex if you use the other one,As other way round you'll have to calculate Tax benifits and Taxable profits and then Tax which is quite complex.

Sir John Correct me if Am wrong.

Thanks in Advance!!

J

John MoffatTutor·

You are correct :-)

N

Nassem·

Thank you :-)

J

John MoffatTutor·

You are welcome :-)

T

Talha·

Hello Sir Lectures are just amazing!

Thing Am confused with is that why we are treating the royalties in both calculations.

1) When calculating Net cash flows(NCF) in Euros

2) When calculating (NCF) in pounds

Why adjustments to be made in both calculations as the cash flows we're converting from have been given the effect of royalty????

Tax effect is understood

J

John MoffatTutor·

The royalties are a cost to the foreign company and income for the home company - it is one way of remitting money to the home country.

While you mentioned that the trick to tackle this is to when you compute the tax allowable depreciation for the purpose of arriving at the Taxable profit in order to figure out the tax expense on the profit, so don’t add back the same after figuring out the tax expense.

However, excluding maintenance expenses when calculating taxable profit can lead to discrepancies in our NPV and cash flow projections. Maintenance expenditure is tax allowable, and it should be kept alongside depreciation before the taxable profit.

For instance, if we were to incorporate maintenance expenses of 1,000 Euro annually in addition to depreciation, it would result in taxable losses, thereby reducing our tax liability. Neglecting these maintenance expenses before arriving at taxable profit inflates the taxable profit figure, consequently leading to higher tax payments.

So why you have not account for the maintenance expenses even it’s cashlfows in your table before arriving the taxable profit?

Just to re-ensure that in case in exam it's being mentioned that an amount equal to the amount of the tax allowable depreciation is required each year for the maintenance of non-current assets. So in such case we wouldn't subtract the maintenance expense to arrive at taxable profit and neither we will add back the tax depreciation after arriving at the taxable cashflows.

However, now do have one more curiosity ? What if in exam it's being mentioned that an amount of XXX (any amount but different to that of depreciation) is required each year for the maintenance of non-current assets. So in such case we would still follow the same treatment as carried out by you?

Furthermore, would take this moment to appreciate your energy for replying to our's queries.

If he had different amount then he would have to make it clear about the tax position.

Thank you for the lectures and notes.

I just had one doubt and that is, in the question its mentioned that "An amount equal to the amount of the tax allowable depreciation is required each year for the maintenance of non-current assets" so for calculating the tax it will be required to deduct the depreciation as well as the maintenance of the same amount from the revenue, that is an amount of 2,000 (1000 for dep, and 1000 for the maintenance). However, as depreciation is non cash it will be returned back. Although, the net effect is same as mentioned but it will definitely affect the tax calculated.

Please explain if i am wrong.

Thank u in advance for clarifying the query.

Was it because the investment was in an operation and not a non-current asset?

Or was it because the operation was not sold/disposed off in Year 5 so there wasn't a balancing charge/allowance?

Or was it due to the straight-line method which doesn't produce a balancing charge/allowance?

As far as the exam is concerned, the residual value is taken to be the sale proceeds.

This is about rounding and rather that typing numers in the CBE versions of the exams, actually using the formula capability of the spreadsheet tool.

Feels like the mark schemes are rounding before the calculations are done.

Do you have any advice, its much quicker and more correct in practice if you dont round a number before calculating.

This problem naturally becomes greater as time periods increase and rely on previous numbers.

Best,

Birju

The marks in Section C are for the approach rather than for the final answer (and nobody cares either in the exam or in real life about a difference of a few hundred).

Thank u very much

Thank you.

With the exams these days taken online using the computers, can we use the calculation options of formulas that the spreadsheet enables, such as =NPV() & =IRR() when calculating NPV etc. or do we still have to use the tables.

Please advise if this is possible or will we lose marks?

Thank you

However for Section A and B questions it is still important that you understand the NPV and IRR.

Let’s say if we decide to add back the TAD within the computation, what plausible assumption that I should state for this. Pls advise.

Then, will the examiner give me the full marks if I don't state the assumption for adding TAD back?

Thanks in advance for your explanation!

If net cash will not be remitted to the UK then what will be the effect on the calculation of NPV? Secondly why we are deducting royalties above as we are making calculations from James Plc's point of view. Please advise.

The royalties are allowed for tax in Obvlivia but are taxable in the UK - the tax rates are different.

In the Oblivia project, why weren't the Maintenance costs also deducted before taxable profits as this is a tax deductible expense and therefore reduce the tax liability? Then after tax calculation, add back the TAD? Although the cash flows would still net off, the tax liability would be different?

Thanks

Thanks :)

I have a question out of curiosity, what will happen if there wouldn't be any double tax treaty in the question?

What will be the tax treatment then?

Thanks for the great lectures.

However in the exam questions there has always been a double tax treaty.

In the UK they pay 25% tax, but because of the double taxation treaty they get credit for the 20% already paid in Oblivia and so just pay an extra 5% to the UK tax authorities.

would there be a 5% tax rebate?

As you mentioned in the previous lecture, investment in a foreign country is different from buying a machine, losses can be carried forward for next year's tax calculation purpose.

Based on above, I have 2 questions regarding example 4

1. why the initial investment of (4545) GBP at time 0's can not be carried forward?

2. if at time 1, we have a loss, can it be carried forward for time 2's tax calculation?

Thank you very much in advance!

2. Yes - a loss at time 1 would be carried forward and reduce the taxable profit at time 2.

what about the 4545 pounds which James Plc is wiring to Oblivia to start this project. Will it not has any tax implications in either UK or Oblivia.If so will it not have an impact on the value of outflow?

I only have one technical question regarding the Notes to the course. I can't find in the Answers section the solutions for Example 4, 5 and 6 under this chapter. I was actually doing a recap and wanted to check against the workings there and that's when i noticed.

Many thanks,

Laura

Thank you for the lecture! Just a question here - why there is a need to add back the depreciation in this case while you did not add back the depreciation in the last example in part 1?

Thanks!!

In example 4, we do not add it back because although it is not a cash flow, the question specifically says that an amount equal to the depreciation is needed for the maintenance of the assets.

As I say in the lecture, this is what the current examiner almost always writes as part of the question.

I am a bit confused regarding depreciation.in the previous eg the depreciation was taken for 4 years wherese in this eg it has been taken for 5 years.

I have already posted a query in ask my tutor forus which i suppose u havent come across.

thanks

I love your way to tutoring

The same rule has been applied in both examples. In Example 1 there is a scrap value at the end of 5 year, and the TAD in the 5th year is the difference between the sale proceeds and the tax written down value.

In Example 4, there is no scrap value (so the sale proceeds are zero) and therefore the TAD is the difference between the tax written down value and zero.

It is stated that the amount equal to the amount of the tax allowable depreciation is required each year for the maintenance of non-current assets.

As I understand this amount is the cash item which Oblivia project has to spent on the FA maintenance. Means, this is the real expenses, which were spent by the company and could be deducted in the tax calculation in addition to TAD.

My Question is: Why during the tax calculation we didn't deduct 20% twice? on tme as TAD, and second time as expenses spent for maintainance

Thanks,

Pave

I am aunable to understand why the TAD is 1000 not 200 as it's generally calc. as

dep*TAD tax rate in this case

5000/5 = 1000*20% =200

Thank you

What you are confusing is that the tax saved as a result of the TAD will be the tax rate (which is 25% and not 20% in the question) as applied to the $1,000,000.

This is happening here - the tax has been calculated on the profit after the TAD.

I will really appreciate if you can help provide some clarification on how to calculate the average inflation rate for the data below.

Expected inflation rates

EU expected inflation rate: Next two years 5%

EU expected inflation rate: Year 3 onwards 4%

USA expected inflation rate: Year 1 onwards 3%

The actual question says "The current selling price of each component is €700 and this price is likely to increase by the average EU rate of inflation from year 1 onwards".

Thanks.

The inflation rates are given in the question - calculating any sort of average rate is of no relevance at all.

If the current price is €700, then the price in 1 year will be 700 x 1.05.

The price is 2 years will be 700 x 1.05^2

The price in 3 years will be 700 x 1.05^2 x 1.03

From then on you multiply by 1.03 each year.

It may help you to watch the Paper FM (was F9) lectures on investment appraisal with inflation.

If the question says "Assume there is no tax relief '' , i believe we tax at their respective rates and not the difference. However, when taxing at the home country, do we tax on taxable profits or the Operating profit ( before capital allowance) ?

A question in the BPP textbook shows that we tax at Operating Profit and not taxable profits. Why so?

I go through all the tax rules for the exam in my lectures.

Please explain the following

A) The concept of Tax saving on Tax allowable depreciation as it was not discussed while solving Example 4

B) The Concept of Double tax treaty: What would have happened if there was no double tax treaty between Uk and Oblivia, We would have then taxed the cashflows as per the respective tax rates in both countries

C) Royalties: Why were they added separately to James plc cashflows when the Cashflows received from Oblivia were already net of the royalty payment to James plc and Why were they taxed at 25 % and not the incremental of 5%

The other way was to calculate the tax after subtracting the TAD, and then add back the TAD because it is not a cash flow. In AFM it is better to use the second way (as I have done in example 4). However the TAD is not added back, because although it is not a cash flow, the question says that an equal amount is needed for the maintenance of non-current assets. I explain about this in the lectures, and as I say in the lecture it is something the current examiner does in all NPV questions.

B. Yes - both sets of flows would have been taxed at the relevant rates. However in every singe exam question a double tax treaty has existed.

C. The royalties are an expense of the company in Oblivia and therefore reduce the Oblivia profits. They are income to James in the UK and are therefore taxed in the UK. This is standard tax rules as well as always being the caae in AFM questions.

Will the examiner always mention that an equal amount Is needed to maintain the non current asset If not can we assume and do our workings according to that?

In Q1 June 2015 named Yilandwe Co, the examiner has first deducted the TAD and then added it back later, The question does not state any thing about the same amount being used to maintain the non current asset. How should we deal such questions?

Thank you.

Guess i simply 'ignored' cash surplus will be remitted to UK each year.

Why is the extra UK tax is calculated by dividing foreign exchange rates when we already converted it into pounds currency in the previous step ?

In example 4, James Pls question we deducted € 1000 depreciation to arrive taxable profit. It’s clear. But shouldn’t we deduct another € 1000 as a maintenance cost to arrive taxable profit ? Question says an amount equivalent to depreciation is required each year to maintain non current assets, so it means in addition to depreciation (non cas expenses) there will be another € 1000 cas out each year for maintenance of non current assets.

Bit concern about the clear treatment as this will be checked in next exam as well

Thanks

Still its not clear on what basis maintanance cost is excluded from the taxable profit calculation. If i include both maintainance and capital allowances for taxable profit calculation in my working will that be incorrect?

why is depreciation is not added back after it is used for tax calculation purposes for the purpose of NPV calculation this is not cash item? As far as I know depreciation is to be used only to reduce taxable base... so following that logic they should be added back.

thanks

The question says 'an amount equal to the amount of the tax allowable depreciation is required each year for the maintenance of non-current assets'. This is something that the current examiner has in most questions.

Therefore although depreciation is not a cash flow and is added back, there is a cash outflow of the same amount. Therefore the net result is no effect.

I do actually explain this in my lecture (because it is coming in the exam these days).

Why has the revenue from royalties been included twice in the answer? The royalty revenues were initially converted into GBP in the earlier part of the answer, and then included again at their GBP amounts.

Thanks, John :)

thank you very much for Your lectures they are very helpful.

I have a question regarding example 4 and the amount payable each year for the maintenance of non-current asset and its treatment for profit or loss purposes.

Could you please advise why they have not been included in calculation of profit? I thought they should be treated as an operating expense (I assume they have not been included in the "Operating costs" line as its amount exceeds the amount disclosed in that item).

Thank you in advance for Your answer

However, since the current examiner always makes the assumption that it is dealt with as I show in my lectures, it would be safest to always assume this :-)

Your lectures are great!

I did not quite get your answer... Would you be able to tell me what the examiner's assumption is? I still cannot see why this is not included in the profit calculation...

Many thanks in advance.

But now you have to use this one to calculate Taxable profits and to apply Tax rate when converting it from one currency to another.

This mathod is easier then the other one as calculations will go complex if you use the other one,As other way round you'll have to calculate Tax benifits and Taxable profits and then Tax which is quite complex.

Sir John Correct me if Am wrong.

Thanks in Advance!!

Thing Am confused with is that why we are treating the royalties in both calculations.

1) When calculating Net cash flows(NCF) in Euros

2) When calculating (NCF) in pounds

Why adjustments to be made in both calculations as the cash flows we're converting from have been given the effect of royalty????

Tax effect is understood