Hi, I have come across a couple pages and examples now in the newest notes you guys provide that are different than what you go through on these lectures. Just an FYI, throws me off course a bit when learning.

Z

Zohaib·

Hey, could someone please tell if these lectures are valid for Dec 2025 attempt?

H

Haider·

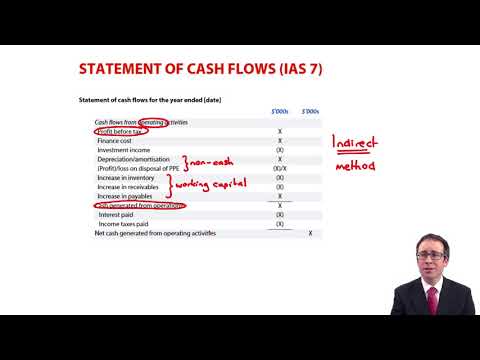

Please explain why Finance Cost is being added back and why investment income is being deducted from the PBT.

J

Jun Wen·

i think it is because for the first portion it is talking about the cash generating from operating activities, so if the P&L already took into considerations for finance cost and investment income, hence we need to reverse them in this section. When we doing the part for cash generated from investing and financing activities, then we will minus and add the cost and income accordingly to calculate the net cash gain/(loss)

A

Amrita·

Good

N

Nickygregory56·

Thanks!

S

shijilroshan·

how finace cost in sopl is credit in t account of intrest payable ?

usualy expense is debit balance right ?

U

ukhan147·

Interest expense is debited in income statement and it also increases the liability so that's why there's a credit in interest payable account.

Journal entry:

Expense- debit(SPL)

Interest payable- credit.(SOFP)

M

mila128·

How come we have to reduce the profit and add the loss on the disposal of the PPE? What is the logic behind it?

Z

zuzer·

the profit or loss on disposal is basically an assumption, since the depreciating element used in arriving the profit or loss. Since the initial adjustment in the SOPL was to add the profit on disposal to the PBT, we have to deduct it from the PBT in the Statement of Cash Flow in order to get the actual profit.

V

viethuynguyen·

i just have a simple understanding that gain increases income and loss reduces income; therefore, in order to see the actual cash flow, we would remove the gain or add back the loss since they are non cash items.

O

olamilakan·

you are right.

P

phyl1998·

There must be a missing video about the 'statement of changes in equity' part. In the note, there is a separate page about SOCE and Chris also mention that at the beginning of this vedio, but we didn't see it either in this or the previous video. Please check it.

T

Tevin·

video on Statement of Changes in Equity not present

E

ezzathassan·

Dear Opentuition

I think there is a missing video related to Statement of change in Equity. as Mr. Chris mentioned at the end of his video

M

MikeLittleTutor·

Because they are items of cash outflows!

P

phyl1998·

There must be a missing video about the 'statement of changes in equity' part. In the note, there is a separate page about SOCE and Chris also mention that at the beginning of this vedio, but we didn't see it either in this or the previous video. Please check it.

C

Chris·

interest paid and tax paid are cash items , why deduction on socf?

P

P2-D2Tutor·

They are payments in cash, and hence deductions given they will have reduced our cash figure.

usualy expense is debit balance right ?

Journal entry:

Expense- debit(SPL)

Interest payable- credit.(SOFP)

I think there is a missing video related to Statement of change in Equity. as Mr. Chris mentioned at the end of his video