There will be a difference in group SFP of 6000/-, which I believe is of investment in PPE.

should we show that 6000 as Bank O.D and tally the SPF.

Is my understanding correct?

W

wasif·

Or I think we should treat it as share capital - 6000/-

Because it's mentioned in question "accounted for it's share of the construction cost".

Help me in understanding this?

Thank you.

P

P2-D2Tutor·

Hi,

You cannot draw up an SFP as you've done above as you do not have a cash balance that has been adjusted following the initial entry to account for the share of the PPE. You need to process the journals and it all will still balance.

Thanks

A

andrew·

hi sir i thought the 600 deprction is supposed to be apportioned based on share holding of 40%

P

P2-D2Tutor·

Hi,

The value of the PPE has already been apportioned and so the depreciation calculated will therefore be apportioned too.

Thanks

L

lakshmi·

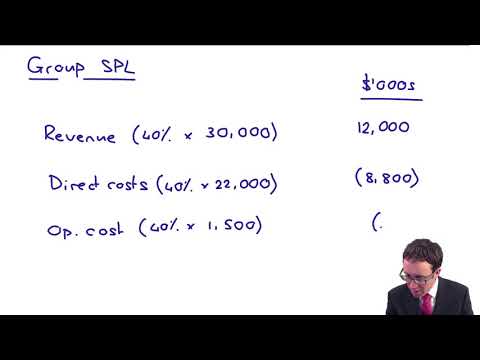

hi sir, i dint quite get the 600 payables added with 8800

and in SPL its 0.6 ... i dont get it .how this 0.6 is come from .show me your working please.

Is there any need to refer study text after referring free videos and open tuition notes

Thanks

Can this be demonstrated by detailing the Dr's and Cr's or is there a need to show the extracts in the FS?

Dr PPE 6

Cr Bank 6

Dr Dep. Costs 0.6

Cr PPE 0.6

Dr Op. Costs 0.6

Cr Payables 0.6

Dr Receivables 12

Cr Revenue 12

Dr Dir Costs 8.8

Cr Payables 8.8

PPE - 5400

Receivable - 12000

Total assets - 17400

Profits(R.E) - 2000

Payables - 9400

Total equity & liabilities - 11,400

There will be a difference in group SFP of 6000/-, which I believe is of investment in PPE.

should we show that 6000 as Bank O.D and tally the SPF.

Is my understanding correct?

Because it's mentioned in question "accounted for it's share of the construction cost".

Help me in understanding this?

Thank you.

You cannot draw up an SFP as you've done above as you do not have a cash balance that has been adjusted following the initial entry to account for the share of the PPE. You need to process the journals and it all will still balance.

Thanks

The value of the PPE has already been apportioned and so the depreciation calculated will therefore be apportioned too.

Thanks

And that 600 has been paid after the year-end